Q1 2026 Luxury Watch Market Report: Submariner Premiums, Nautilus Trends and What It Means for Co-Ownership

Q1 2026 Luxury Watch Market Report: Submariner Premiums, Nautilus Trends and What It Means for Co-Ownership

The secondary luxury watch market just posted its strongest quarter since the 2022 correction. After nearly two years of declining values and cautious sentiment, Q1 2026 marks a clear turning point for structured access to non-bankable assets.

The Recovery Is Real

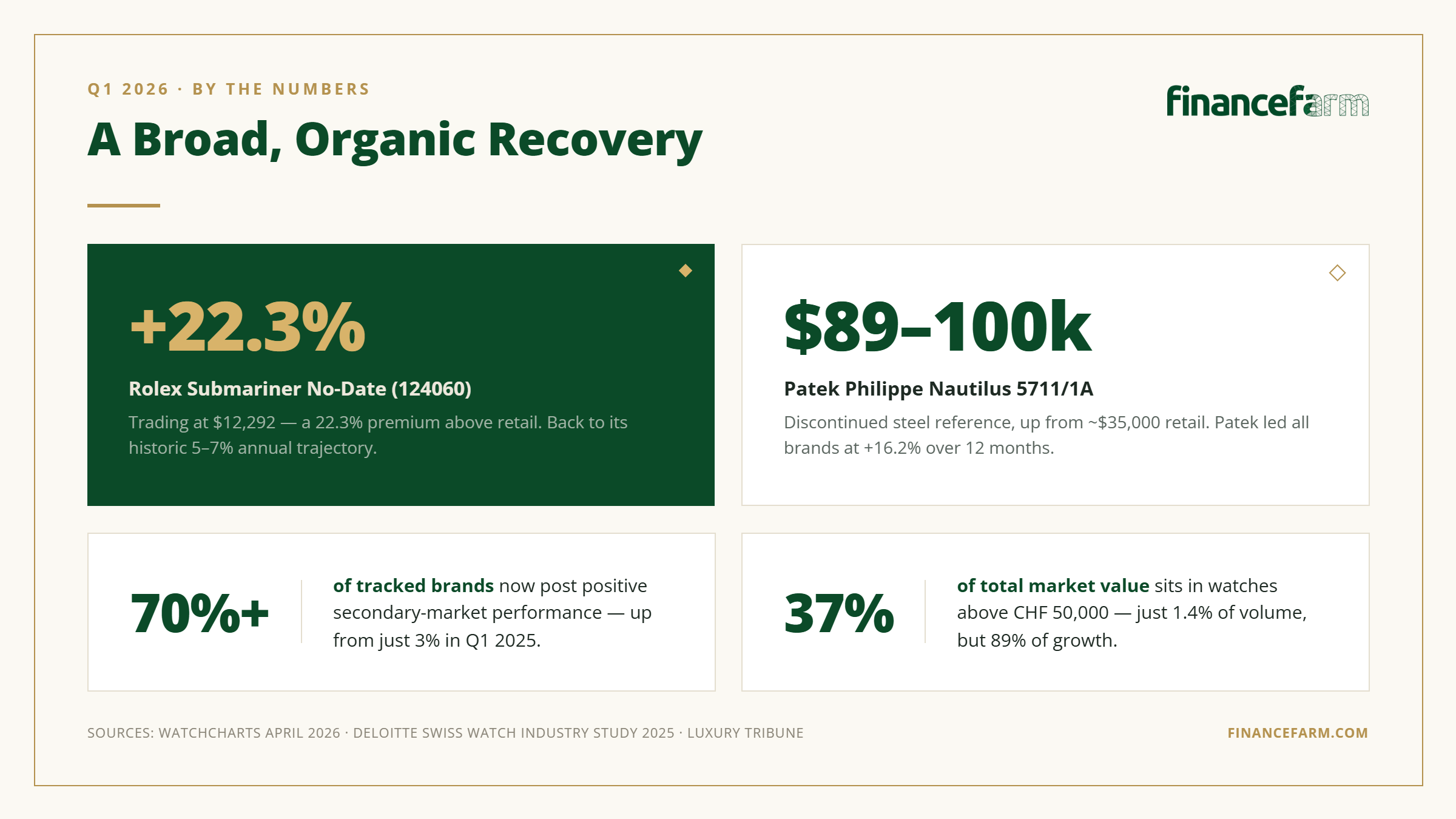

According to the WatchCharts Overall Market Index, the secondary watch market gained +8.2% over the past 12 months as of April 2026. Monthly data confirms steady momentum: January posted +0.8%, February +0.6%, and March cooled slightly at +0.1%.

The most significant shift is in breadth. Over 70% of tracked watch brands are now posting positive secondary market performance, up from just 3% in Q1 2025 (WatchCharts April 2026 Market Update). Recovery has been led by the "Big Three" of Rolex, Patek Philippe, and Audemars Piguet, with the broader market following.

Unlike the speculative bubble of 2020 to 2022, this recovery appears organic. Demand is driven by informed collectors and pre-owned buyers rather than flippers.

Rolex Submariner: Premiums Have Stabilized

The Submariner remains the benchmark for accessible luxury watch appreciation. Current secondary market pricing as of April 2026 shows the Submariner No-Date (Ref. 124060) trading at $12,292, a 22.3% premium above its $10,050 retail price (WatchCharts, Ermitage Jewelers).

The discontinued "Hulk" (Ref. 116610LV) continues to trade at roughly double its original retail price, benefiting from its status as a permanently closed set. Historically, Submariner references appreciate at an average of 5 to 7% annually, and Q1 2026 data confirms a return to that trajectory after the speculative spike of 2021 to 2022.

No new Submariner was announced at Watches and Wonders 2026, though industry signals point to a possible blue ceramic bezel variant arriving later in 2026.

Patek Philippe Nautilus: The Blue-Chip Benchmark

Patek Philippe led all brands in Q1 2026 performance, posting a +1.2% gain in March alone and a cumulative +16.2% over the past 12 months (WatchCharts, Luxury Tribune).

The discontinued steel Nautilus 5711/1A, originally retailing at approximately $35,000, now commands $89,000 to $100,000 on the secondary market. The current production 5811/1G in white gold retails at $89,767 and trades above $150,000 (Luxury Watches USA).

Waitlists for new Nautilus references now exceed 8 years at authorized dealers, and steel variants sell 40% faster than gold or platinum on the pre-owned market.

The Broader Market Is Polarizing

The Swiss watch industry is experiencing significant structural polarization. According to the Deloitte Swiss Watch Industry Study 2025, watches priced above CHF 50,000 represent just 1.4% of total volume but account for 37% of total value and 89% of growth.

The "Big Four" brands (Rolex, Cartier, Audemars Piguet, and Patek Philippe) now control nearly 50% of the total market. Meanwhile, gold prices have surged past $5,000 per ounce as of January 2026, reinforcing the hard asset backing of luxury timepieces.

What This Means for Structured Co-Ownership

Three key takeaways emerge from the Q1 2026 data.

First, the market has stabilized. With over 70% of brands in positive territory, co-ownership models benefit from predictable, data-driven environments rather than speculative volatility.

Second, scarcity drives premiums. Discontinued references like the Submariner Hulk and the Nautilus 5711/1A consistently command the highest secondary market premiums. When production stops, supply is permanently fixed and demand only grows. These are precisely the types of assets that structured co-ownership platforms target.

Third, the secondary market is becoming the primary market. Gen Z and informed buyers are increasingly choosing pre-owned over retail waitlists (Deloitte 2025). This structural shift creates sustained demand for the types of assets held and rotated within co-ownership structures.

FinanceFarm's predefined minimum safety margin ensures that co-participants are protected even during corrections, because acquisition pricing already accounts for downside risk.

Sources Cited

- WatchCharts Market Index Reports, January to April 2026

- Deloitte Swiss Watch Industry Study 2025, 11th Edition

- Federation of the Swiss Watch Industry (FH) Export Data, Q1 2026

- Ermitage Jewelers Pricing Data, April 2026

- Luxury Tribune Market Analysis, April 2026

- Watches and Wonders 2026 Coverage, Geneva, April 14 to 20

Comments ()

No comments yet

Be the first to share your thoughts!