What Are Non-Bankable Assets? A 3-Minute Guide

Banks won't touch them. Auction houses charge 26% in fees. Yet non-bankable assets represent one of the largest and most resilient pools of wealth on the planet.

Here is what the data actually says, and why the access story is finally changing in 2026.

Definition: what a non-bankable asset actually is

A non-bankable asset is a tangible valuable that your bank cannot accept as collateral, custody on your behalf, or include in a standard portfolio report. Luxury watches. Fine art. Rare collectibles. Fine wine. Precious coins. Raw materials.

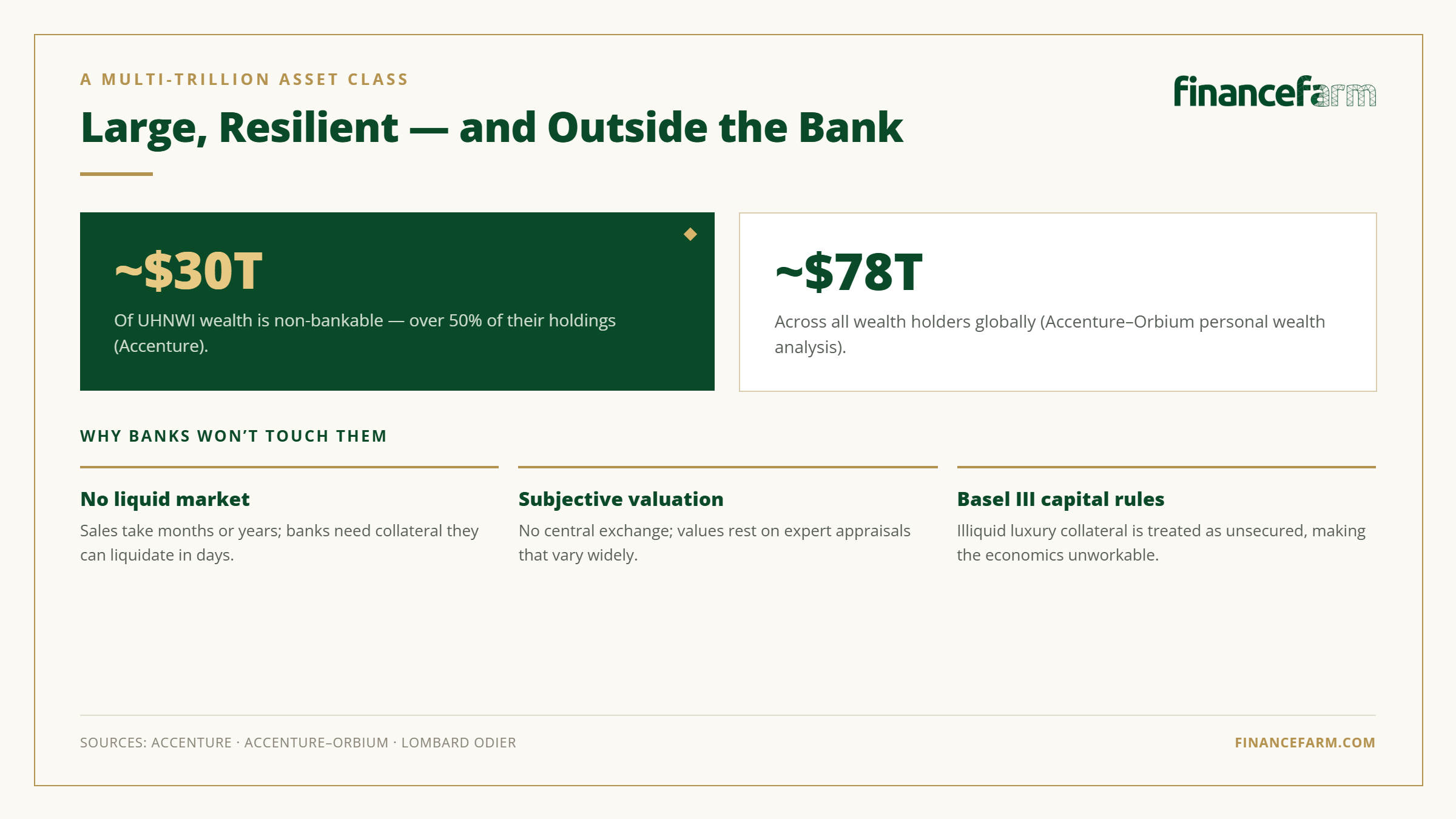

The category is not small. According to Accenture, more than 50% of all assets held by ultra-high-net-worth individuals globally are non-bankable, equating to approximately USD 30 trillion. Broaden the lens to all wealth holders and the global figure climbs to roughly USD 78 trillion, per a joint Accenture-Orbium analysis of global personal wealth.

That is a multi-trillion dollar asset class that sits almost entirely outside the banking system.

The problem: why banks won't touch them

Three structural barriers keep non-bankable assets out of the traditional banking framework.

No liquid market. Selling a luxury asset can take months or years. Banks require collateral they can liquidate in days. A 1968 Patek Philippe, a Basquiat canvas, or a case of 1982 Domaine de la Romanée-Conti cannot be sold overnight at a predictable price.

Subjective valuation. There is no centralised exchange for most of these assets. Values depend on expert appraisals, which can vary significantly between professionals. As Lombard Odier's wealth planning team notes, luxury assets frequently sit outside standard bankable frameworks, making them vulnerable to regulation differences across jurisdictions.

Basel III regulation. Post-financial-crisis banking rules treat loans collateralised by illiquid luxury assets as effectively unsecured. That means banks must hold prohibitively high capital reserves against them, which makes the economics unworkable for all but a handful of specialist private banks.

The result: a structurally excluded asset class.

Performance: yet they outperform most traditional asset classes

This is the part most people never see.

The Knight Frank Luxury Investment Index tracks a weighted basket of 10 collectible asset classes across a decade. Its long-term numbers speak for themselves.

Luxury watches led the index with a 125.1% increase over the past ten years, according to the 2025 KFLII. Fine art, rare coins, fine wine and coloured diamonds all delivered meaningful appreciation across the same period.

Zoom out further and the story gets stronger. As Liam Bailey, Knight Frank's global head of research, put it: a USD 1 million allocation to the index in 2005 would now be worth USD 5.4 million, compared with USD 5 million for the same amount placed in the S&P 500 by the end of 2024.

Three properties drive that performance. Low correlation with public equities. Genuine tangibility as a store of value. And resistance to inflation that paper assets rarely match.

The cost: the hidden fees of trading them

So if the numbers are this strong, why does almost nobody own them?

Because the auction house economics are brutal.

Christie's current fee schedule charges a 26% buyer's premium on the first USD 1 million of hammer price, plus 21% on the portion up to USD 6 million, and 15% above that. Sotheby's briefly attempted a simpler flat 20% model in 2024, then reverted to a 27% buyer's premium on works up to USD 1 million from February 2025.

That is the buyer side. The seller side adds another 10% to 15% commission on most consignments. Stack insurance, shipping, and VAT on top, and the combined transaction cost on a single trade can easily exceed 35% of the hammer price.

For anyone building a serious position, those fees compound quickly. A 125% ten-year appreciation looks very different after two rounds of auction friction.

The solution: non-bankable assets deserve a better marketplace

The appetite has never been the problem. Family offices have quietly held watches, art and wine for generations. High-net-worth collectors allocated an average of 20% of their wealth to art in 2025, up from 15% in 2024, according to Art Basel and UBS.

The problem has always been infrastructure. Three centuries of auction house dominance, opaque pricing, and regulation that treats luxury assets as unbankable have kept ordinary wealth builders structurally locked out.

FinanceFarm is building the structured investment infrastructure that changes this. Transparent pricing. Lower transaction fees. A Swiss-structured framework. Institutional grade processes applied to an asset class that has operated without them for too long.

Non-bankable assets are not a new idea. They are one of the oldest and most resilient stores of value in human history. What changes in 2026 is simply who gets to own them.

Comments ()

No comments yet

Be the first to share your thoughts!