Why Selling Through FinanceFarm Beats Auction Houses. A Data-Driven Comparison

You own a CHF 80,000 Patek Philippe Aquanaut. You want to convert it into liquidity. So you start weighing your options.

You could consign it to an auction house and wait months for the right sale season, hoping bidders show up and your reserve is met. You could take it to a private dealer and negotiate a price with no comparable data and no visibility into how they arrived at their number. You could walk into a pawn shop or asset-backed lender and borrow against it at double-digit interest rates, knowing you lose the watch if you miss a payment.

Or you could submit it to FinanceFarm.

Each of these options involves trade-offs. The question is not which one gives you the highest possible sale price in a best-case scenario. The question is which one gives you the most certainty, the fastest timeline, the lowest risk of failure, and the cleanest process. When you look at the data, the answer becomes clear.

What Auction Houses Actually Charge

The auction fee structure is more complex than most sellers realise when they first consign a piece. There are two sides to it: what the buyer pays and what the seller pays. Both come out of the same transaction, and both reduce what you actually receive.

On the buyer side, premiums at the major houses have climbed steadily for decades. As of early 2024, Sotheby's restructured its buyer premium to a flat 20% on hammer prices up to $6 million and 10% above that, according to Sotheby's own announcement. Christie's maintained a tiered structure that starts at 26% on the first million and steps down from there, as reported by The Art Newspaper. By early 2026, Sotheby's reversed course and reinstated a tiered premium structure, with rates reaching 28% on lower value lots according to the same source. Phillips introduced its own restructured fee schedule in September 2025.

These buyer premiums matter to you as a seller because they inflate the total cost for the person acquiring your asset. A bidder willing to pay CHF 80,000 for your watch is actually committing CHF 96,000 or more once the premium is added. That changes bidding behaviour, suppresses final hammer prices, and means your asset may sell for less than it would in a market without that overhead.

On your side as the seller, the standard commission runs around 10% to 15% of the hammer price, depending on the house and the lot value. According to MyArtBroker's guide to auction fees, sellers also face additional charges for insurance (often called loss, damage, and liability coverage), shipping, photography, and catalogue placement. These are negotiable in theory, but in practice only sellers with high value consignments have the leverage to push back.

If your lot does not sell, you still owe an unsold lot fee. And the market now knows your piece failed to find a buyer at the price you set. That is reputational damage that follows the asset into its next attempt at sale.

There is also the question of access. The major auction houses are selective about what they accept. If your asset does not meet their internal thresholds for value, category fit, or sale calendar timing, they may decline your consignment entirely or direct you to a lower profile online-only sale with minimal marketing support. For sellers with mid-range assets, the doors to a Christie's or Sotheby's live sale may simply not open. FinanceFarm does not operate on prestige gatekeeping. If your asset has verified market data and clean provenance, you can submit it through the app regardless of whether an auction house would have accepted it.

Add it all up. On a CHF 80,000 watch that hammers at estimate, the buyer may pay CHF 96,000 or more. You receive CHF 68,000 to CHF 72,000 after seller commission and fees. The auction house and its fee structure have consumed somewhere between 25% and 35% of the total transaction value. And that is the good outcome. If the lot goes unsold, you receive nothing and still owe fees.

What Pawn Shops and Asset-Backed Lenders Offer

This is the option sellers turn to when they need cash fast and do not want to wait for an auction cycle. Asset-backed lenders and pawn shops will give you liquidity against your watch, artwork, or collectible, typically within days. But the terms are punishing.

Interest rates on asset-backed loans for luxury goods typically run between 12% and 30% annually. The lender takes physical custody of your asset. If you miss a payment, you lose the watch. Miss two and they sell it, often well below market value, to recover their capital quickly. You have no control over the exit price and no recourse once the asset is liquidated.

The fundamental problem is that this is not a sale. It is debt secured against your property. You do not receive liquidity. You receive a liability. And the lender's entire model depends on the possibility that you will default, at which point they acquire your asset at a fraction of its value.

There is also no transparency in how the loan-to-value ratio is determined. The lender sets the valuation, the terms, and the timeline. You take it or leave it.

How FinanceFarm Works Differently

FinanceFarm is neither an auction house nor a lender. It is a structured acquisition platform.

When you submit an asset, FinanceFarm's valuation team assesses it using a proprietary multi-stage process that includes provenance verification, condition assessment, comparable market analysis, and internal modelling of liquidity indicators and seasonal patterns. If the asset qualifies, FinanceFarm makes you a direct purchase offer.

Here is the critical difference in how the economics work. FinanceFarm applies a predefined minimum safety margin on every acquisition. That means the company acquires assets at a significant discount to the most recent verified sale price. On a watch with CHF 80,000 in verified market value, the offer you receive will be meaningfully below that figure. This is by design. The safety margin is what makes the entire model work. It creates structural downside protection for the co-participants who later acquire fractional co-ownership shares on the platform, and it is the reason FinanceFarm can offer sellers something no auction house or pawn shop can: absolute certainty of outcome.

You will not receive CHF 80,000 for that watch. But here is what you will receive: a clearly defined amount, with zero seller fees deducted, paid out in full once the participation round closes and funds are confirmed. No commissions. No listing fees. No insurance charges. No unsold lot penalties. The price quoted is the price received. Every time.

The trade-off is straightforward. You accept a lower price than the theoretical maximum you might achieve at auction. In return, you get speed, certainty, zero fees on what you receive, full digital processing, blockchain verification, and the option to buy your asset back later if you change your mind.

The Timeline Problem

Fees and pricing are only part of the equation. The other part is time.

Auction houses operate on seasonal calendars. The major watch sales at Christie's, Sotheby's, and Phillips happen in May, June, November, and December. If you approach an auction house in January, the earliest realistic slot is May. That is four to five months of waiting before the gavel even falls. If the piece does not sell, you are looking at the November cycle. That is nearly a year from your first phone call.

Pawn shops are faster, but you are not actually selling. You are borrowing. The clock starts ticking on interest payments immediately, and the pressure to repay only increases over time.

FinanceFarm operates on a different rhythm entirely. Once you submit your asset through the app, the compliance review and valuation process can produce a clear offer within days. If you accept, the purchase contract is e-signed digitally, the asset is inspected, and it enters the platform. The entire seller journey from submission to payout runs through four digital phases with no seasonal dependency.

Your asset does not need to wait for the right auction season. It does not need a printed catalogue. It does not need a preview exhibition. It needs verified market data, clean provenance, and a physical inspection that matches your documentation. That is it.

Transparency: What You See vs What You Get

One of the most persistent complaints from auction sellers is the gap between the estimate they are given at consignment and the amount that actually lands in their bank account.

The estimate is not a guarantee. It is a marketing range designed to attract bidders. The actual hammer price can land above, below, or within that range, and there is no way to predict it. Once you add buyer premium on top (which the seller does not receive) and subtract seller commission, insurance, and fees from underneath, the final number can be dramatically different from what the seller expected.

According to Knight Frank's Wealth Report 2025, auction lots in 2024 achieved only 70% of their high estimate on average, down from 87% in 2021. That means the estimate you were shown at consignment may have overstated the likely outcome by 30% before fees were even applied.

Pawn shops offer a different kind of opacity. The loan-to-value ratio is set by the lender with no obligation to explain how they arrived at the number. There is no comparable data shared, no methodology disclosed, and no second opinion available.

FinanceFarm removes ambiguity on both sides. The valuation is evidence-based, grounded in FinanceFarm's proprietary internal process that analyses comparable market data across multiple verified sources. The offer you receive is not a range. It is a specific number. And that number is what you get paid. There is no gap between the estimate and the outcome because they are the same thing.

Every step of the transaction is documented on the blockchain. Purchase price, costs, sale proceeds, and payouts each receive an on-chain timestamp that cannot be altered after the fact. Your dashboard in the app shows the live status of every deal. This is not a black box. It is a glass one.

The Risk You Do Not Talk About at Auction

There is a risk baked into the auction model that rarely gets discussed at the consignment stage: the risk of a buy-in.

A buy-in happens when your lot fails to reach its reserve price and goes unsold. According to industry data, buy-in rates at the major houses fluctuate between 20% and 35% depending on the category and the state of the market. In a softening market like the one observed across 2023 and 2024, those rates climb.

When your lot is bought in, three things happen. First, you owe an unsold lot fee. Second, the auction result is now public record, and any subsequent attempt to sell the same piece carries the stigma of a failed sale. Third, you have spent months in the consignment process with nothing to show for it.

Pawn shops carry their own version of this risk. If you default on your loan, the lender liquidates your asset at whatever price clears their books. You lose the asset and any equity above the loan amount disappears with it.

FinanceFarm does not have buy-in risk because the model is fundamentally different. FinanceFarm acquires your asset directly, subject to its predefined minimum safety margin. If your asset qualifies and you accept the offer, the transaction proceeds. There is no auction. There is no reserve price. There is no public failure scenario. There is no debt to service. You sell the asset. You get paid.

The Buy-Back Option: Something No Other Channel Can Offer

Here is something no auction house, no dealer, and no pawn shop in the world can give you. If you sell your asset through FinanceFarm and later decide you want it back, you can repurchase it within the agreed window.

The premium you pay covers the return earned by the co-participants who held co-ownership shares in the meantime. It is a clean, predefined structure. You know the terms before you sell. And if your circumstances change, you have a path back to your asset.

Try asking Christie's for a buy-back clause on your consignment. The conversation will be short. Try asking a pawn shop to return your watch after they have sold it to recover a defaulted loan. It is already gone.

Who Should Still Use an Auction House

This is not a blanket argument against auctions. There are situations where an auction house is the right choice.

If you hold a once-in-a-generation masterwork with global museum interest, the competitive bidding environment at a Christie's evening sale can achieve prices that no other channel will match. The Paul Allen collection sale in November 2022 at Christie's generated over $1.5 billion. A Patek Philippe Grandmaster Chime sold at Sotheby's for CHF 31 million. These results happen at auction because the scarcity and prestige of the lot creates its own demand.

But the vast majority of sellers are not consigning pieces at that level. For those sellers, the fee structure, timeline, uncertainty, access barriers, and risk of a buy-in make the auction model significantly less attractive than a structured, fully digital alternative with a defined outcome.

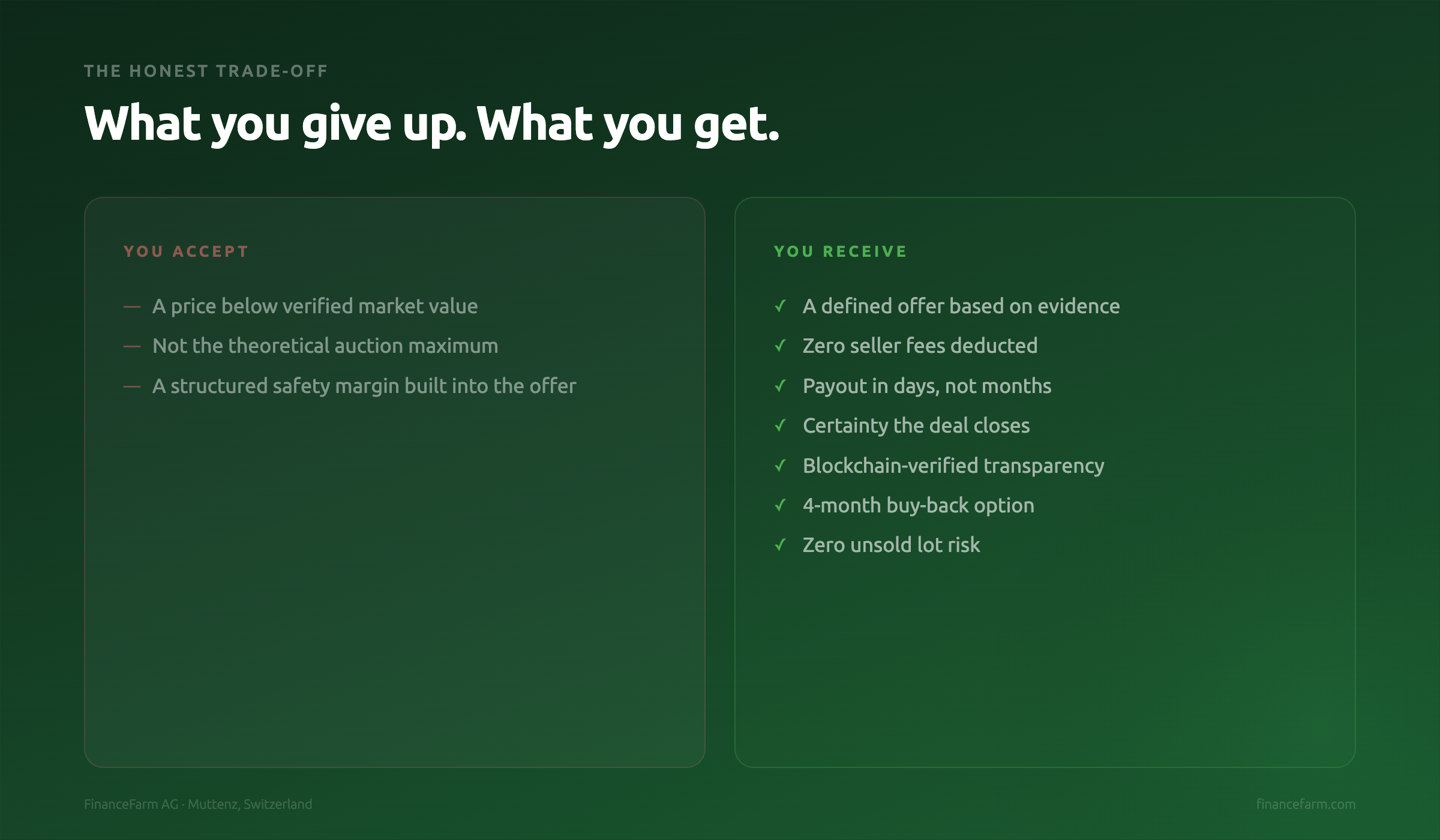

The Honest Trade-Off

FinanceFarm is not claiming you will receive more money than you would at auction in a best-case scenario. The predefined safety margin means the acquisition price sits below the asset's verified market value. That is the trade-off, and it is built into every deal.

What you receive in exchange for that trade-off is worth understanding clearly. You get a defined offer based on evidence, not a speculative estimate. You get zero seller fees deducted from your payout. You get a digital process measured in days, not months. You get certainty that the deal will close once you accept the offer. You get blockchain-verified transparency at every step. You get the option to buy your asset back later. And you completely eliminate the risk of an unsold lot, a failed auction, or a debt obligation.

For many sellers, that combination is worth more than the theoretical possibility of a higher hammer price that may or may not materialise, after fees that may or may not have been fully disclosed at consignment.

The Market Is Shifting

The secondary market for luxury assets is evolving rapidly. Online transactions now account for a growing share of all sales. Chrono24 processes over 600,000 verified watch transactions tracked through its ChronoPulse index, with over nine million users visiting the marketplace monthly. At the major auction houses, more than a third of purchasers at Sotheby's 2024 New York day sales acquired their lots online, as noted in Knight Frank's Wealth Report 2025.

The infrastructure for digital transactions in high value tangible assets is no longer theoretical. It exists. FinanceFarm is building the version of that infrastructure specifically designed for sellers who want certainty, speed, transparency, and a defined outcome.

Think Your Asset Qualifies?

If you hold a luxury watch, fine art, a rare collectible, or a raw material with verifiable market value and clean provenance, you can submit it for a free evaluation. No commitment. No fees. Blockchain-verified. Swiss-regulated.

Start your submission at financefarm.com/become-seller

FinanceFarm AG | Muttenz, Switzerland

This content is for informational purposes only and does not constitute financial advice. Target returns are based on the business model and are not guaranteed. All participation in co-ownership carries risk.

Comments ()

No comments yet

Be the first to share your thoughts!