Why Non-Bankable Assets Need a New Solution And What FinanceFarm Is Building

There is a strange contradiction at the heart of the luxury market.

A Patek Philippe Nautilus can sell for three times its retail price on the secondary market. A Basquiat painting that traded privately in 2012 for $16 million went under the hammer five years later for $110 million. Rare Scotch whisky has outperformed the S&P 500 over the last decade. These are not speculative bets. They are categories with verified transaction histories, passionate global buyer bases, and strong long term appreciation. Yet walk into any bank in Zurich, London, or New York with a CHF 200,000 Rolex Daytona on your wrist and ask them to recognise it as collateral. They will politely decline.

Not because the watch has no value. But because their systems were never designed to handle it. No standardised pricing model. No custody framework. No liquid exchange where the asset can be converted to cash at the push of a button.

This is the non-bankable asset problem. And it is not small. The Knight Frank Luxury Investment Index tracks ten categories of tangible collectibles, from watches and wine to art and classic cars, and estimates the combined global market at well over three trillion dollars. That is trillions in real, proven, appreciating value sitting outside the financial system because no one built the infrastructure to bring it in.

Until now. FinanceFarm was built specifically to solve this.

The Options That Exist Today (and Why They Fall Short)

If you own a high value tangible asset and want to convert it into liquidity, you currently have three paths. None of them are good.

Auction Houses

The most visible option. Christie's and Sotheby's are household names, and for works above a certain value, they remain a relevant channel. But the economics are brutal. Buyer premiums at the major houses now run between 20% and 28% on the hammer price, depending on the tier. Seller commissions typically sit at 10% to 15%, with additional charges for insurance, shipping, photography, and catalogue placement. By the time both sides have paid their fees, the effective transaction cost can reach 25% or more of the sale price. And that is before you account for the timeline. Consigning a piece to a major auction means waiting for the right sale season, which could be months away. There is no guarantee the item will meet its reserve. If it does not sell, you get it back with a bill for the unsold lot fee and the market now knows your piece failed to find a buyer. That is not a problem that helps your negotiating position next time.

Private Dealers

The alternative for sellers who want discretion. A private dealer or gallery will find you a buyer, usually through their personal network, and take a commission in the range of 10% to 20%. The problem is opacity. You have almost no visibility into how the price was determined, how many potential buyers were contacted, or whether the dealer is also representing the other side of the transaction. Pricing is based on relationships, not evidence. And timelines remain unpredictable.

Short Term Collateral Lenders

A growing category, particularly in the watch and fine art space. These firms will lend you cash against your asset, typically at annual interest rates between 12% and 30%, with the asset held as security. Miss a payment and you lose the watch. Miss two and they sell it, often below market value, to recover their capital. This is not structured liquidity. It is a pawn shop with a website.

Why the Market Stays Broken

The common thread across all three options is fragmentation. There is no single platform that handles the full transaction lifecycle for non-bankable assets. Valuation is done by one party. Sales by another. Settlement by a third. Custody sits somewhere else entirely. Every step introduces a new intermediary, a new fee, and a new opportunity for delay or information asymmetry.

Compare this to equities. When you sell a share of stock, the entire process from order to settlement runs on a single integrated infrastructure. Price discovery, matching, execution, and transfer all happen in seconds, with complete transparency at every step. The non-bankable asset market has nothing comparable. It operates the way the stock market did before exchanges existed: through private negotiations, handshake agreements, and a lot of trust in the right people.

FinanceFarm is building the infrastructure layer that this market is missing.

How FinanceFarm Actually Works

The model is straightforward, but the discipline behind it is what makes the difference.

FinanceFarm acquires tangible, non-bankable assets at a steep discount to their verified market value. The company applies a predefined minimum safety margin on every acquisition. If a comparable asset recently sold for CHF 100,000 at auction or through a verified private transaction, FinanceFarm will only acquire it at a fraction of that value. There are no exceptions to this rule. It applies to every watch, every artwork, every collectible that enters the platform, regardless of category or ticket size. This is not diversification. It is structural downside protection built into every single deal, before anyone else participates.

Once the asset is acquired, it is tokenised. Each asset is represented digitally in the FinanceFarm app, and co-ownership shares are made available to buyers as child NFTs on the Arbitrum blockchain. This is not speculative token trading. Each NFT is backed by a specific, identifiable physical asset that is held, insured, and managed by FinanceFarm throughout the entire process.

The asset then enters one of FinanceFarm's structured rotation strategies. D-3 runs on an approximate three month cycle with a 10% target return and is available selectively for corporate clients. D-6 is the core product, rotating co-ownership positions in roughly six months with a 20% target return. D-9 extends to approximately nine months with a 25% target return, used for assets where a longer marketing window unlocks additional value. There is also the Buy-Back option, a fixed return structure with a maximum four month term, designed for buyers who prefer predictability over variable outcomes.

During the rotation, the asset is marketed through the platform's in-app co-participation feature. When the asset sells, the co-ownership is economically transferred to the third party buyer, and you are paid out in full according to the deal terms. You claim your payout directly in the app, where the smart contract handles the allocation automatically.

That is the full cycle. Acquisition, tokenisation, participation round, sale, payout. Then the capital is free to enter the next rotation.

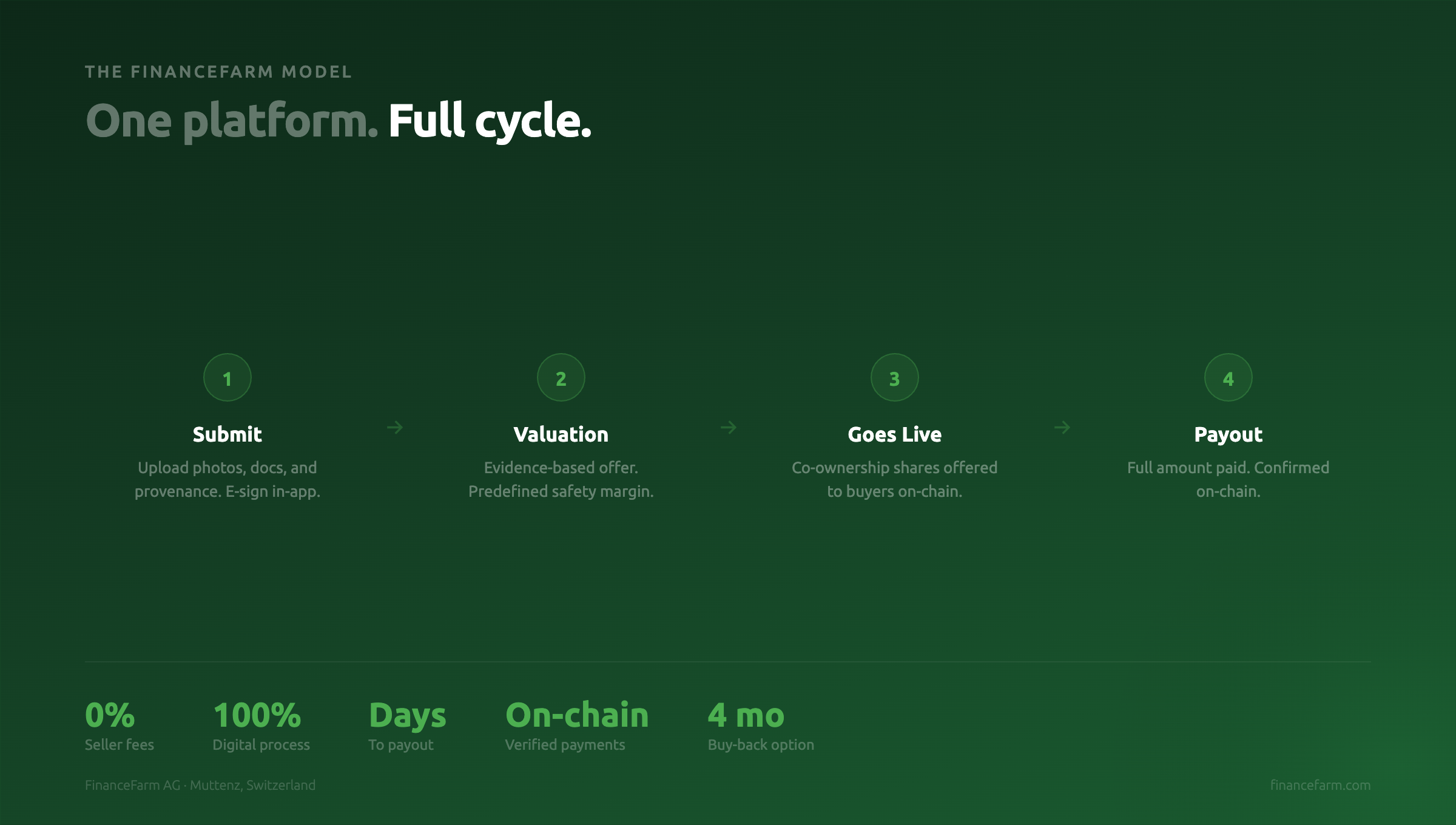

The Seller Experience: Four Phases, Fully Digital

If you own a luxury watch, a piece of fine art, or a collectible that you want to liquidate, the traditional process is slow, opaque, expensive, and uncertain. FinanceFarm replaces all of it with a single digital workflow. The entire seller journey runs through four clear phases in the app.

Phase 1: Submit Your Asset

You start by creating a case in the app. You select the category, describe the item, upload the required photos into defined slots, and provide supporting documents and provenance details. You then e-sign declarations confirming ownership and legal source of the asset. Once everything is complete, you submit the file and the system freezes it as an immutable snapshot. That snapshot becomes the single source of truth for everything that follows. No ambiguity, no back and forth. If something is missing, the app tells you before you can submit.

Phase 2: Valuation and Agreement

FinanceFarm's compliance team reviews your submission against the frozen snapshot. They assess provenance, condition, documentation quality, and market comparables. If anything needs clarification, they request it directly through the app and you respond in the same flow. Once the review is approved, FinanceFarm prepares your purchase agreement. You and FinanceFarm both e-sign the contract in the app, and the asset undergoes a physical inspection to confirm it matches what was submitted. There are no seller fees. No commissions deducted from your payout. No hidden charges for photography, insurance, or listing. The price you are quoted is the price you receive.

Phase 3: Your Asset Goes Live

Once compliance approval, a signed contract, and confirmed inspection are all in place, your asset goes live on the platform. Co-ownership shares are offered to buyers who can acquire fractions through the app. The participation round runs for a defined window, and you can track progress in real time through your seller dashboard. Push notifications and platform communications are triggered automatically, but only after all prerequisites are met. Your asset is never listed before the full process is complete.

Phase 4: Participation Closes, You Get Paid

Your payout is released only after the participation round closes successfully and funds from the buyers have been received and reconciled. This is a strict, gate-based process. Even if your listing is live and participation is at 99%, no payout is triggered until the round is fully closed and funds are confirmed. The payout then goes through a multi-step internal approval process before it is executed and you are notified in the app.

There is also a buy-back option. If you sell your asset to FinanceFarm and later decide you want it back, you can repurchase it within the agreed window. The premium you pay covers the return earned by the buyers who held co-ownership shares in the meantime. It is a clean, transparent structure that gives you a path back to your asset if circumstances change.

Think about how different that is from calling a dealer, waiting for a callback, negotiating a price with no comparable data, hoping the cheque clears, and wondering whether you left money on the table.

The Protections That Make It Work

Structured products only deserve the name if the structure actually protects the people involved. FinanceFarm has built several layers of protection into every deal, and they are non-negotiable.

The predefined minimum safety margin is the starting point. Every acquisition must clear this threshold, which means the margin potential exists before a single buyer participates. This is not diversification. Diversification spreads risk across positions. The safety margin eliminates the need for the asset to appreciate at all in order to generate a return.

Every payment, from acquisition through to payout, is confirmed on-chain. The blockchain timestamp cannot be altered after the fact, which means there is a complete, immutable audit trail for every deal. Funds are held in segregated accounts specific to each deal. They are never pooled with FinanceFarm's operating capital or mixed between transactions.

All material decisions follow a four-eyes principle. No single person approves a high-impact acquisition alone. Risk appetite, target holding period, and exit corridor are defined before any purchase. The portfolio is diversified across asset classes, geographies, and ticket sizes, with larger positions split across multiple rotations to manage concentration risk.

All transactions are processed in compliance with KYC and AML requirements, with verification automatically triggered once daily activity reaches USD 1,000.

Who This Is For

FinanceFarm serves two specific groups exceptionally well.

For asset sellers: if you hold a high value tangible asset and want a fast, transparent, fully digital process that does not charge you seller fees, does not leave you waiting for the right auction season, and gives you a verifiable valuation backed by data rather than a phone call, FinanceFarm is the alternative you have been looking for.

For buyers: if you want structured, repeatable access to real world assets with defined rotation timelines, a built-in safety margin on every deal, and full blockchain transparency from start to finish, this is the platform that was designed for that purpose.

Both groups benefit from the same underlying principle. When every transaction runs through a single platform with standardised processes, evidence-based valuations, smart-contract governance, and on-chain verification, the entire experience becomes faster, cheaper, and more trustworthy than any combination of traditional intermediaries.

The Market Is Ready. The Infrastructure Is Here.

For decades, non-bankable assets have been trapped in a system that was never designed for them. Banks will not touch them. Auction houses take months and a quarter of the value. Private dealers operate behind closed doors. Collateral lenders charge predatory rates and hold your asset hostage.

FinanceFarm does not patch one part of this broken system. It replaces the entire cycle with a single, transparent, blockchain-verified platform. From seller submission to buyer payout, every step is digital, every valuation is evidence-based, every payment is confirmed on-chain, and every deal carries a predefined structural safety margin.

This is structured liquidity for the world's most valuable tangible assets. Built in Switzerland. Available in the app.

Ready to sell your asset on your terms?

Start your submission at www.financefarm.com

Comments ()

No comments yet

Be the first to share your thoughts!